Understanding the Substantial Presence Test: Are you a nonresident for tax purposes?

Understanding the Substantial Presence Test: Are you a nonresident for tax purposes?

When you live, study, or work in the U.S. on a temporary visa, your tax status is not decided by your visa alone. One of the most important rules the IRS uses is the Substantial Presence Test (SPT). Misunderstanding this test is one of the most common reasons nonresidents file the wrong tax return.

At J1 Summer Tax Back, this is one of the first areas we help clients understand, because getting your residency status wrong can lead to penalties, incorrect tax bills, or missed refunds. That’s why J1 Summer Tax Back places such a strong emphasis on explaining the Substantial Presence Test clearly and practically.

What is the Substantial Presence Test?

The Substantial Presence Test is an IRS rule used to determine whether a non-U.S. citizen should be treated as a resident alien or a nonresident alien for tax purposes.

If you meet the test:

- You are treated as a U.S. resident for tax purposes

- You must report worldwide income

- You usually file Form 1040

If you do not meet the test:

- You are treated as a nonresident alien

- You generally report only U.S.-sourced income

- You usually file Form 1040-NR

At J1 Summer Tax Back, we see many people assume they are nonresidents just because they hold a visa like J-1 or F-1. The IRS does not work that way. Days matter, and J1 Summer Tax Back makes sure those days are counted correctly.

How to calculate the Substantial Presence Test

To meet the Substantial Presence Test, both of the following conditions must be satisfied:

- You were physically present in the U.S. for at least 31 days in the current tax year, and

- You were present for 183 days or more over the last three years using this weighted formula:

- All days in the current year count as 1 full day

- Days in the previous year count as ⅓ of a day

- Days in the year before that count as ⅙ of a day

Example calculation

- 120 days in the current year → 120 × 1 = 120

- 180 days in the previous year → 180 × ⅓ = 60

- 210 days two years ago → 210 × ⅙ = 35

Total = 215 days

Because 215 is greater than 183, this person meets the Substantial Presence Test and is considered a U.S. resident for tax purposes.

This is exactly the kind of scenario J1 Summer Tax Back reviews carefully, because even small miscalculations can completely change your filing obligations.

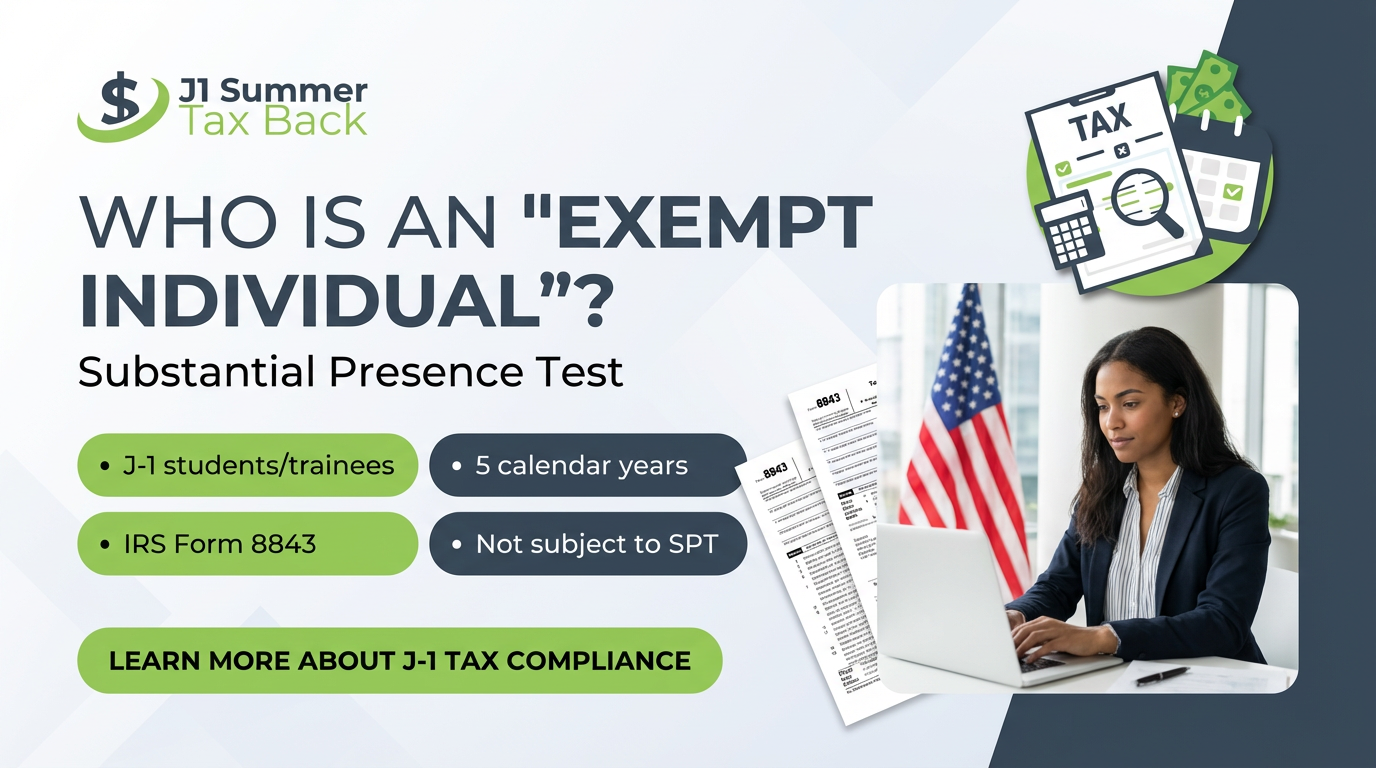

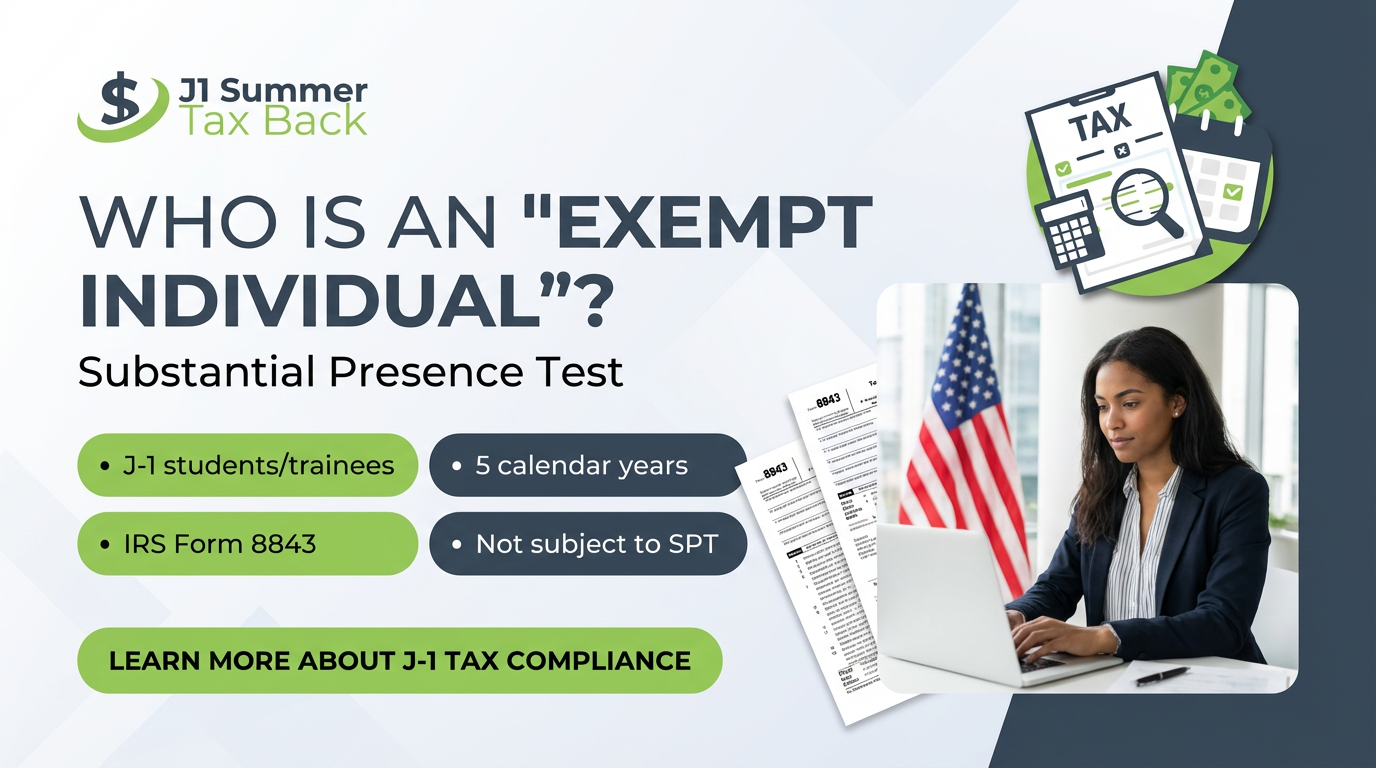

Who is an “exempt individual” for the Substantial Presence Test?

Certain visa holders are classified as exempt individuals, meaning their days do not count toward the Substantial Presence Test for a limited period.

These include:

- F-1 and J-1 students (generally exempt for up to 5 calendar years)

- J-1 scholars, teachers, and researchers (generally exempt for up to 2 calendar years)

- Certain diplomats and foreign government employees

- Professional athletes competing in charitable events

Important:

“Exempt” does not mean exempt from tax filing. This is a common misunderstanding that J1 Summer Tax Back corrects all the time. It only means exempt from counting days toward the test.

Real-world case examples

F-1 student

An international student on an F-1 visa in their third year in the U.S. is usually still a nonresident alien for tax purposes. They normally file Form 1040-NR, something J1 Summer Tax Back helps with frequently.

J-1 researcher

A J-1 researcher may be exempt for two years, but once that exemption ends, days start counting. J1 Summer Tax Back often sees people accidentally continue filing as nonresidents after this point, which can cause serious IRS issues.

H-1B worker

H-1B visa holders do not receive an exemption. If they meet the 183-day rule, they are residents for tax purposes. J1 Summer Tax Back regularly helps workers transition correctly between filing statuses.

Switching from F-1 or J-1 to H-1B

This is one of the most complex scenarios. Days that were previously exempt can suddenly start counting mid-year. J1 Summer Tax Back specializes in identifying exactly when that switch changes your tax residency.

The Closer Connection Exception

Even if you meet the Substantial Presence Test, you may still avoid resident status if:

- You spent less than 183 days in the U.S. in the current year, and

- You can prove a stronger connection to another country

In this case, Form 8840 must be filed with the IRS. This is another area where J1 Summer Tax Back provides step-by-step support, as mistakes here are common.

Substantial Presence Test vs. Green Card Test

The Substantial Presence Test is based on days.

The Green Card Test is based on status.

If you hold a U.S. green card, you are automatically a resident for tax purposes, regardless of how many days you were physically present. J1 Summer Tax Back always checks both tests to determine the correct outcome.

Why the Substantial Presence Test matters so much

Your result affects:

- Which tax return you file (1040 vs 1040-NR)

- Whether worldwide income must be reported

- Eligibility for deductions, credits, and treaties

- Your risk of IRS penalties

This is why J1 Summer Tax Back treats residency determination as the foundation of correct tax filing.

Final thoughts

The Substantial Presence Test is one of the most important — and most misunderstood — U.S. tax rules for nonresidents. Whether you are on a J-1, F-1, H-1B, or another visa, counting days correctly can mean the difference between compliance and costly errors.

At J1 Summer Tax Back, we help you determine your correct tax residency, file the right forms, and avoid unnecessary problems with the IRS — all while ensuring you don’t pay more tax than legally required. 40

Start using our services by selecting the right service for your case here: https://j1summertaxback.com/service-selector