Hiring J-1 Employees

A Complete Guide to Employer Tax Requirements

Picture this. It is your busiest week of the season and a new group of J-1 staff arrives ready to work. Payroll needs to set them up fast, managers want them on the schedule, and the employees are anxious because they have never been paid in the U.S. before. If tax withholding is set up incorrectly on day one, the problem usually shows up later as an angry employee, a delayed refund, or a request to correct a W-2.

This guide explains what U.S. employers need to know to handle J-1 employee tax compliance correctly from the start, using plain language and the right nonresident rules.

Can an employer hire someone on a J-1 visa

Yes, if the individual is authorized to work for your organization as part of their J-1 program. J-1 Exchange Visitor categories include Summer Work Travel, Intern, Trainee, Camp Counselor, Au Pair, Teacher, Research Scholar, Physician, and others. Work authorization depends on the program category and sponsor rules, so the employer’s first step is confirming the employee’s work authorization documents and program details.

Key employer takeaway

A J-1 employee is not hired like a standard U.S. resident employee. Visa category and program sponsor constraints affect work eligibility, payroll treatment, and tax forms.

Step 1: Determine the employee’s tax residency status

Your payroll withholding depends heavily on whether the employee is a nonresident alien for tax purposes.

Most J-1 participants are nonresidents for tax purposes during an initial “exempt individual” period. In many common J-1 categories, days in the U.S. may be excluded from the Substantial Presence Test for a limited number of calendar years. After that period, some J-1 workers can become residents for tax purposes based on their days of presence.

What employers should do

- Ask the employee for their U.S. entry history and J-1 category.

- Use a residency determination process that applies the Substantial Presence Test correctly, including any exempt individual rules.

- Reassess residency if the employee returns for multiple years.

Why it matters

If you treat a nonresident as a resident, you can withhold incorrectly, mishandle treaty benefits, and issue the wrong type of reporting forms.

Step 2: Understand what taxes apply to J-1 nonresident employees

Federal and state income tax

J-1 nonresident employees generally owe U.S. federal income tax on U.S. wages. State income tax may also apply, depending on the state where the work is performed.

FICA taxes for J-1 nonresidents

Many J-1 nonresident employees are generally exempt from Social Security and Medicare taxes (FICA) when their work is permitted under their visa and they remain nonresidents for tax purposes.

Common problem

FICA is sometimes withheld by mistake, especially when the employee is entered into payroll as a standard U.S. worker.

If FICA was withheld in error

Employers typically correct this through payroll correction procedures and may need to issue a corrected wage statement (Form W-2C) when required. Employees often cannot easily recover incorrectly withheld FICA without employer involvement.

Important note

FICA exemption is not automatic in every scenario. If a J-1 employee becomes a resident for tax purposes, the FICA exemption can change. Always base payroll treatment on confirmed residency status.

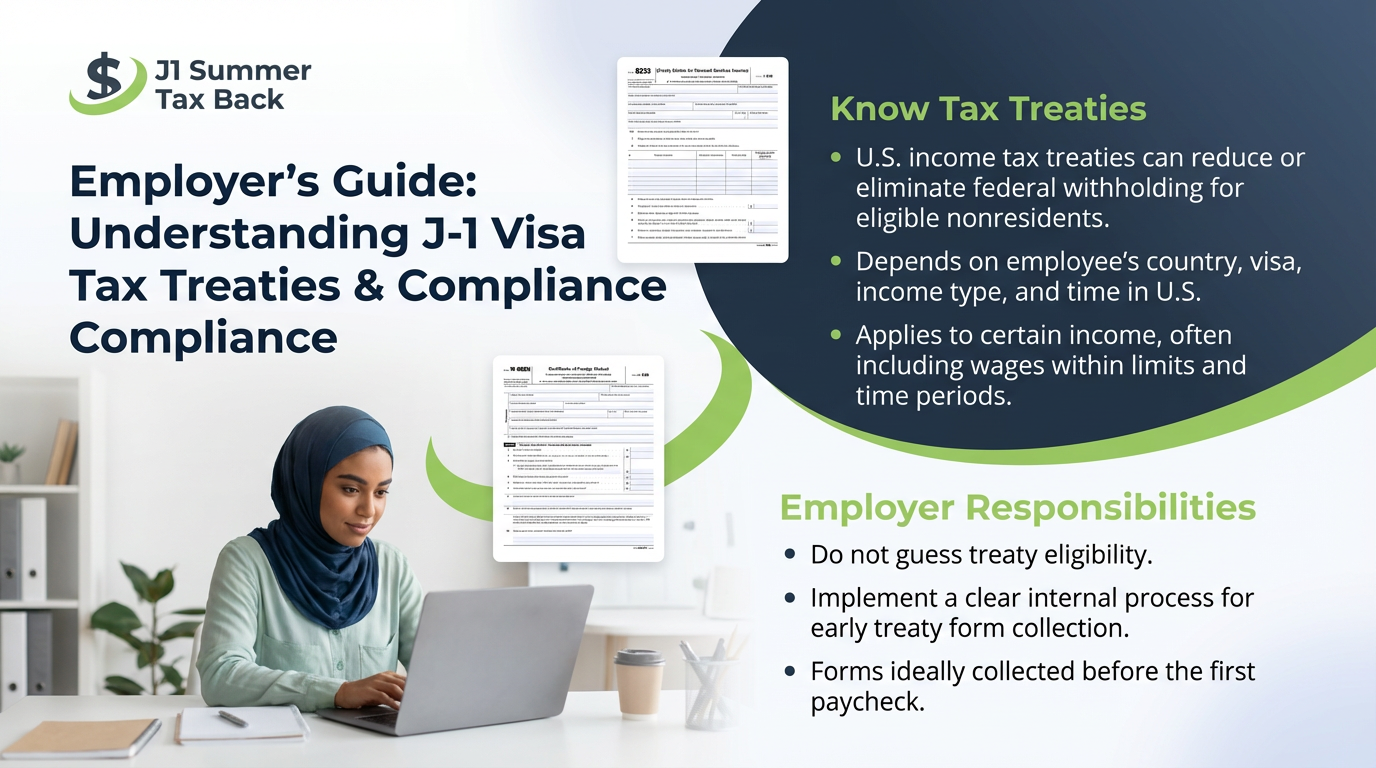

Step 3: Know tax treaties and what employers need to do

The U.S. has income tax treaties with many countries. Some treaties can reduce or eliminate U.S. federal income tax withholding on certain types of income for eligible nonresident employees, often including wages within limits and time periods.

Employer responsibilities

- Do not guess treaty eligibility. It depends on the employee’s country, visa type, income type, time in the U.S., and the treaty article.

- Put a clear internal process in place to collect treaty forms early, ideally before the first paycheck.

Two common treaty related forms employees may provide

- Form 8233 for treaty claims on personal services income, such as wages

- Form W-8BEN for certain non wage income types or to certify foreign status in specific payment situations

Step 4: Collect the right forms at onboarding

A clean onboarding process prevents most nonresident withholding errors.

Form W-4

J-1 employees should complete Form W-4 so you can calculate federal income tax withholding. Nonresident W-4 completion has special IRS rules that differ from resident employees. If you follow resident W-4 logic, you can underwithhold or overwithhold.

Employer best practice

Train HR and payroll to recognize nonresident W-4 requirements and to flag any entries that look like resident filing patterns.

Form 8233 (if claiming a treaty on wages)

If a treaty wage exemption applies, the employee may submit Form 8233. Employers typically must follow IRS procedures for reviewing and submitting the form within required timeframes and retaining copies.

Form W-8BEN (in applicable payment situations)

This may be used in situations involving certain non wage payments or to claim treaty benefits for specific income categories. Many regular payroll wage situations rely on Form 8233 instead, so the correct form depends on the payment type.

SSN or ITIN

Employees are often in process of obtaining an SSN. If they are not eligible for an SSN, an ITIN may be needed for tax filing. From an employer standpoint, your focus is ensuring you collect the correct identification information and maintain accurate payroll records, while the employee handles the IRS application when required.

Step 5: Issue the correct year end tax documents

Form W-2

Employees need a W-2 to file their U.S. tax return, typically Form 1040-NR for nonresidents. The W-2 must reflect correct wage and withholding amounts. Errors often trigger refund delays or IRS correspondence.

Common employer timeline

Provide Form W-2 by January 31.

Correcting mistakes

If withholding or reporting errors are discovered later, you may need to correct payroll records and issue Form W-2C when appropriate. This is especially important for FICA errors.

A practical checklist for employers hiring J-1 workers

- Verify work authorization tied to the J-1 program and sponsor rules

- Determine tax residency status correctly, then document your determination

- Configure payroll for nonresident withholding rules

- Identify whether a tax treaty may apply and collect the proper treaty paperwork before the first paycheck

- Confirm FICA exemption eligibility for J-1 nonresident employees and prevent incorrect FICA withholding

- Maintain clear records and deliver year end forms accurately and on time

- Correct errors quickly using payroll correction procedures and corrected forms when needed

Why this matters for your J-1 employees

For many J-1 participants, U.S. payroll and tax forms are completely new. When employers withhold incorrectly or issue incorrect documents, the employee often feels stuck, especially after they return home. A correct setup from day one helps them file a compliant nonresident return, claim treaty benefits when eligible, and receive the refund they are entitled to without unnecessary delays. 4

Start using our services by selecting the right service for your case here: https://j1summertaxback.com/service-selector